Christie's Sold $2.7 Billion in Art Secretly Last Year. Here's Why That Should Alarm You.

How the Art Market's Private Auction Turns Perfect the Architecture of Speculation, and Why Secrecy Without the Custodian's Contract Is Only Darkness

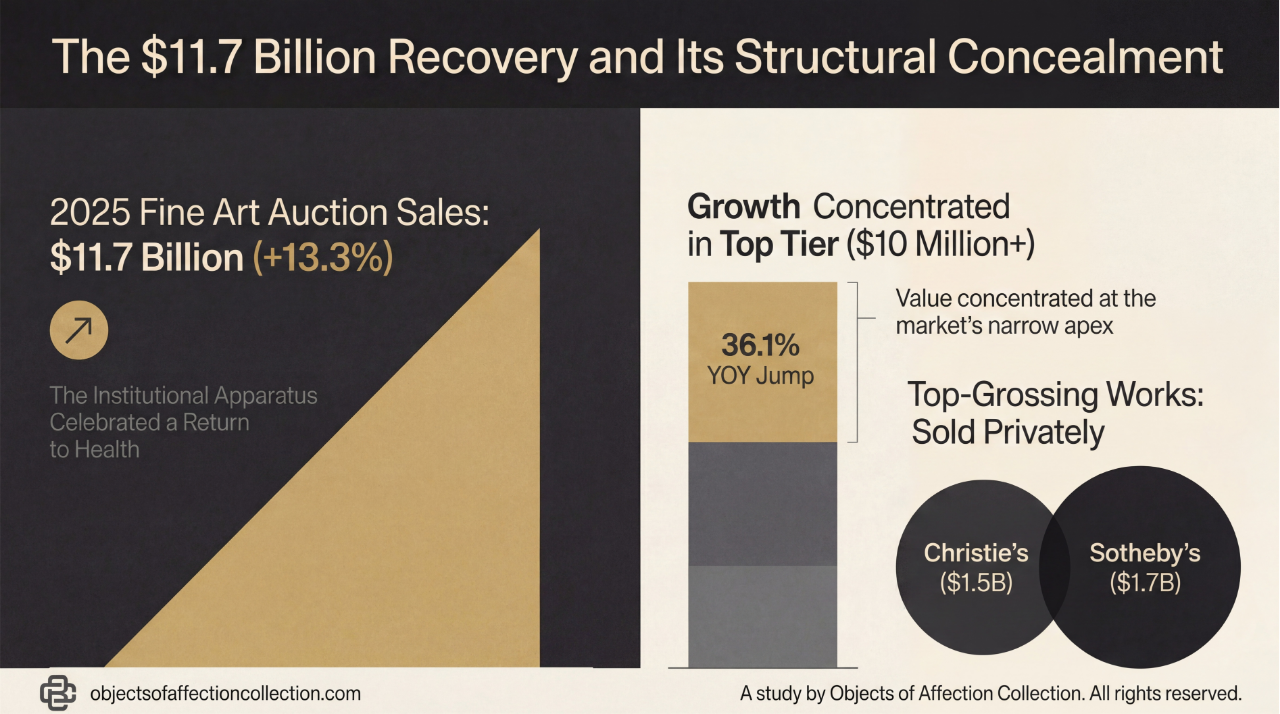

Fine-art auction sales rose 13.3% to $11.7 billion in 2025, and the institutional apparatus celebrated. But the Art Market's recovery narrative conceals a structural migration that the headline figure cannot explain: the wholesale flight of the ultra-wealthy from the public saleroom into invitation-only Private Auction environments. Christie's secret invite-only sales—including reported transactions for a Rothko at approximately $195 million and a van Gogh at approximately $200 million—and the emergence of Fair Warning's Dark Mode format at Clemente Bar represent not an evolution of the market but the refinement of its most ancient pathology: the conversion of art into a privately transacted Hollowed Object. This study deploys the PLCFA critical lexicon—specifically Anti-Speculative Autonomy, Custodian's Contract, Anti-Sale Covenant, Zero-Sum Aura, Speculative Capital, and Semantic Burden—to diagnose the private auction turn as an upgrade of speculation's operating system, not its abolition. Secrecy is not stewardship. Exclusivity is not ethics. The darkness of Dark Mode is not the darkness of the Monastic Veto; it is the darkness of the vault. This study names the difference and proposes what genuine post-speculative institutional architecture requires.

THE $11.7 BILLION RECOVERY AND ITS STRUCTURAL CONCEALMENT

When Artnet reported that fine-art auction sales had risen 13.3% to $11.7 billion in 2025, the institutional apparatus invoked the language of health. The Art Market had stabilized. The Spectacle had returned. The brief that The Tyranny of the Archive demolished still circulates at cocktail hours: the market recovered.

Structural Concealment: While the headline $11.7 billion figure suggests health, the data reveals a radical migration into "Dark Mode" environments where value is extracted in total secrecy.

What the headline conceals is architectural. Of the $11.7 billion, growth was concentrated almost entirely in the $10 million-and-above tier—a 36.1% year-over-year jump to $2.3 billion, representing works numbering in the hundreds, not the thousands. Ultra-contemporary art—the speculative frontier that defined the 2021–2022 boom—contracted by nearly 70% from peak. The Financialization of Luxury did not reverse. It elevated. It tightened. It removed itself from public view.

Simultaneously—and this is the structural fact the headline cannot hold—Christie's disclosed that its three top-grossing works in 2025 were sold not in any saleroom, but privately. Sotheby's private sales reached $1.2 billion. Christie's private sales reached $1.5 billion. Combined, the two houses moved nearly $2.7 billion in art without a paddle, a lot number, a public estimate, a recorded result, or a witness outside the room.

“The 2025 recovery is not a return to health. It is the perfection of concealment. The market did not come back into the light. It learned to operate permanently in the dark.”

This is not a corruption of the market. It is the market's logical destination, absent structural intervention. The Speculative Capital that has governed the art world since at least the 1980s has always required opacity to function. Public auctions were always a theater—a price-discovery mechanism whose real function was not discovery but confirmation: the legitimization of values that had already been privately negotiated. Dark Mode is not the market's betrayal of the public interest. It is the public interest's absence made manifest.

The Theater of Confirmation: Traditional public auctions serve as a spectacle of legitimization for values often negotiated long before the first paddle is raised.

THE ANATOMY OF DARK MODE: WHAT FAIR WARNING FORMALIZED

On November 19, 2025—while Christie's main saleroom was mid-auction at Rockefeller Center—a small group of market insiders left the building and walked to Clemente Bar at Eleven Madison Park. There, Loïc Gouzer's Fair Warning platform conducted an invitation-only auction for a single work: Andy Warhol's Brigitte Bardot (1974). Estimated at $8–12 million. It sold for $16.7 million. The guests were hand-picked. The result produced no public estimate, no public challenge period, no public loss rate. Only a number—and the status it conferred on everyone in the room.

Gouzer describes his model as a hybrid: the competitive dynamic of the auction married to the discretion of the private sale. This framing is precise and revealing. Secrecy, exclusivity, and the theater of bidding—but only for those who have already been screened, approved, and invited. The competitive dynamic is preserved not as a market mechanism but as an experience architecture. It makes the high bidder feel the friction of competition without ever exposing their identity, their tax situation, or their portfolio strategy to outside scrutiny.

Christie's version is more architecturally developed and more structurally consequential. The house launched its invite-only private auction format in 2021 and has conducted—by their own account—a "good handful" of such events. Reported transactions include a Frida Kahlo at more than $150 million, a Mark Rothko No. 6 at approximately $195 million, and a van Gogh at approximately $200 million. These are not supplementary revenue streams. These are price-setting events conducted outside the market's only accountability mechanism—the public record.

“Christie’s private auction format does not protect the collector from the market. It protects the market from the collector’s right to know.”

The structural danger is not that prices are high. High prices for canonical works are a symptom, not a cause. The structural danger is that these prices are being set in an environment with no Provenance Integrity requirement, no Moral Weight Per Material assessment, no public challenge to the claimed provenance, and no mechanism by which subsequent custodians can know the ethical history of what they are being offered. The Hollowed Object circulates in darkness, accruing transactional value while hemorrhaging Semantic Burden.

THE WHALE ECONOMY: THIRTY PEOPLE AND THE ARCHITECTURE OF ZERO-SUM AURA

Ask any major auction house how many whales—the ultra-wealthy collectors capable of moving the top tier—are active in the international market, and the answer is consistent: approximately thirty. Philip Hoffman, CEO of the Fine Art Group, has said it plainly. Market veterans repeat it as an article of faith. The entire architecture of the private auction economy—the secrecy, the invitation protocols, the 365-day Dark Mode selling that trade publications now document as the industry's primary growth strategy—is designed around the preferences of fewer people than fit in a corporate boardroom.

This concentration is the purest expression of Zero-Sum Aura in the contemporary market. The aura of these works does not grow with each transaction; it contracts. Every private sale removes a quantum of public meaning from the object. Every invitation-only environment further narrows the population capable of witnessing, challenging, or contextualizing the work's value claims. The Sign Value that Jean Baudrillard identified as the market's primary commodity is not created through private transactions—it is extracted from the public archive of meaning that makes the work legible in the first place.

The whale economy is a Necrophagy operation. It does not generate new meaning. It consumes the accumulated cultural significance that decades of public scholarship, institutional exhibition, critical writing, and curatorial labor have deposited in the object—and converts that accumulated significance into a private price point, inaccessible to the public infrastructure that created it. The $195 million Rothko was not worth $195 million because a small group of invited bidders valued it at $195 million. It was worth $195 million because Mark Rothko spent his life in genuine conversation with abstraction, because museums housed his work at public expense, because curators wrote about it, because students studied it, because the public meaning accumulated over seventy years of institutional attention created a foundation upon which a private number could be placed.

“Dark Mode does not bypass the public aura. It feeds on it. The whale economy is the parasitic structure that the market built to consume the meaning it never paid for.”

This is what The Tyranny of the Archive named as financial necrophagy: the system cannibalizing its own historical archive to produce the optics of health. Dark Mode is necrophagy made methodology. It is the market formalizing, systematizing, and operationalizing its capacity to extract value from the public cultural record while systematically excluding the public from any claim on the results.

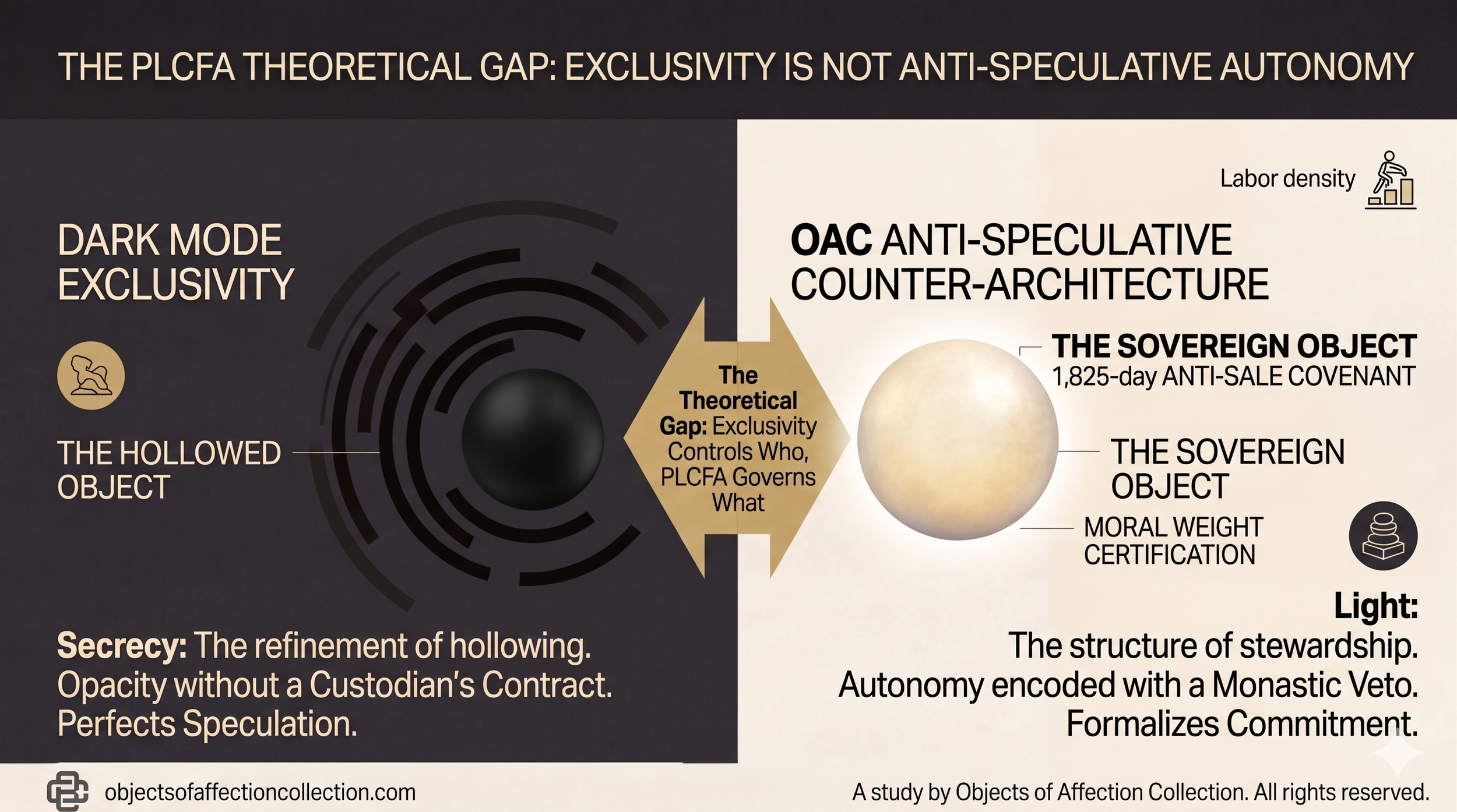

THE PLCFA THEORETICAL GAP: EXCLUSIVITY IS NOT ANTI-SPECULATIVE AUTONOMY

The critical misreading that the private auction turn invites is the equation of secrecy with stewardship. If the public auction was the problem—the spectacle, the media coverage, the status theater, the guaranteed lots and third-party financial instruments—then the private environment, the argument runs, must be the solution. No spotlight. No press. No estimate battles. Just serious collectors making serious decisions about serious works.

The Theoretical Gap: Exclusivity merely restricts access; the PLCFA framework governs the object's future through the Anti-Sale Covenant and Custodian's Contract.

This misreading is structurally fatal. The problem with the public auction was never the publicity. The problem was—and remains—the absence of any Anti-Speculative Autonomy architecture: any mechanism by which the object's future could be governed by something other than the preferences of whoever outbid everyone else in the room. Transferring that mechanism from a public room to a private one does not alter its logic. It perfects it.

The Custodian's Contract—OAC's foundational legal instrument—is absent from every private auction transaction. The whale who wins the invitation-only bidding has no obligation to the work beyond whatever the standard sale agreement encodes. They may sell it tomorrow, hold it in freeport storage for a decade, or offer it to the next Dark Mode auction as soon as the market conditions favor it. The work has acquired a new price. It has not acquired a new custodian. There is no instrument binding the buyer to the object's ethical trajectory, display obligations, or community accountability.

The Anti-Sale Covenant—the PLCFA mechanism by which the artist encodes a temporal lock on the object's resale—is similarly absent. The Monastic Veto, as deployed in the OAC's own Anti-Sale Covenant with a 1,825-day prohibition, demonstrated that this architecture is not theoretical. It has been enacted. It operates. But it operates in contradiction to the private auction economy, which requires liquidity—the perpetual capacity to price, move, and reprice the object—as its operational foundation.

“The private auction is the speculative economy with better manners. It maintains every structural feature that produces the Hollowed Object—the transactability, the opacity, the absence of custodial obligation—while adding a velvet rope.”

This is the PLCFA theoretical gap the private auction turn exposes: the entire apparatus of Dark Mode exclusivity is oriented toward protecting the Speculative Capital of the transaction—shielding it from market scrutiny, tax exposure, and reputational risk—not toward constituting the buyer as a genuine custodian. The Patronage Validation that comes from signing a Custodian's Contract, accepting display obligations, and agreeing to an Anti-Sale Covenant is precisely what the private auction format is designed to prevent. It wants the buyer's capital. It does not want the buyer's commitment.

THE SOTHEBY'S SEALED PARADOX: DEMOCRATIC OPACITY

Sotheby's has pursued a complementary architecture: the Sealed sale, a hybrid online format where screened participants bid without seeing the full competitive landscape, knowing only their top-three position. What began with four to six cars per year has become monthly. The format has expanded to art and jewelry, with mixed results—a Yoshitomo Nara failed to sell in Hong Kong—but the structural logic is consistent with the Christie's model: to extract the competitive energy of the auction while removing its primary accountability mechanism, the public record.

Sotheby's Sealed adds a democratizing veneer to the opacity logic. Unlike Christie's invite-only events, which are explicitly constructed around the approximately thirty ultra-wealthy collectors who drive the top tier, Sealed sales are theoretically accessible to any screened buyer who can demonstrate payment capacity. The velvet rope is a credit check rather than a relationship. The exclusivity is financial rather than social.

But the structural result is identical. A Hollowed Object moves from one owner to another through a process in which its Moral Weight Per Material is never assessed, its custodial obligations are never formalized, its Anti-Sale trajectory is never encoded, and its Narrative Permanence is never guaranteed. The transaction is fast, opaque, and liquid. The object remains, as it has always been in the speculative economy, fundamentally unowned—held without obligation, circulated without commitment, priced without accountability.

“Sotheby’s Sealed democratizes access to opacity. It makes the Hollowed Object available to a slightly wider pool of buyers. It does not make the buyer a custodian.”

This is the distinction the market cannot make without the PLCFA framework. Exclusivity and Anti-Speculative Autonomy are not the same category. The former controls who enters the transaction. The latter governs what the transaction constitutes. A sealed or invite-only environment can be used to execute the most purely speculative transaction in the market's history. The opacity serves the speculator as much as it serves the custodian—perhaps more, because the speculator benefits from the absence of a public record to challenge their claims.

THE SINGAPORE PROTOCOL AND THE ANTI-SPECULATIVE COUNTER-ARCHITECTURE

The diagnosis of Dark Mode as speculative perfection is not a counsel of despair. The counter-architecture is already operational. The Singapore Protocol—OAC's study of the 72-hour non-response of sophisticated Banksy holders following the AP citation event—demonstrated that the most serious collectors in the contemporary market do not move when the speculative pressure intensifies. They hold. And they hold not because they cannot sell, but because they have, consciously or intuitively, constituted themselves as custodians rather than speculators.

The Silent 95—the overwhelming majority of significant Banksy holders in the Singapore market who did not liquidate following the Reuters unmasking—enacted what the PLCFA framework formalizes as Anti-Speculative Autonomy: the refusal to allow the speculative logic of the transaction to govern the object's future. They did not hold because they lacked information. They held because they possessed something the private auction economy cannot supply: a relationship with the object that was not reducible to its current price.

This relationship—the Custodian's relationship—is what the Custodian's Contract formalizes. It does not restrict the collector. It constitutes them. A collector who signs a Custodian's Contract accepting display obligations, community access provisions, and Anti-Sale Covenant terms has not constrained their collection. They have elevated it. They have moved from holding assets to holding obligations—from owning objects to stewarding them.

“The answer to Dark Mode is not more light on the transaction. It is the Anti-Sale Covenant attached to the object before it enters any transaction environment, public or private.”

The OAC's own Anti-Sale Covenant—a 1,825-day prohibition encoded in a private commission as documented in The Named Ghost: Part II—is not a philosophical aspiration. It is a deployed precedent. It demonstrates that the Monastic Veto operates at the highest level of custodial consciousness before it ever reaches institutional policy. The counter-architecture to Dark Mode does not require reforming the auction houses. It requires the systematic deployment of instruments—Custodian's Contract, Anti-Sale Covenant, Moral Weight Certification—that survive transfer and travel with the object regardless of the transaction environment.

SEMANTIC BURDEN AND THE OBJECT THAT REFUSES TO BE HOLLOWED

The Semantic Burden of an object is not its price. It is the accumulated weight of its making: the material choices, the labor density, the ethical provenance, the community accountability, the documented history of human contact. A Rothko at $195 million in a private room carries an enormous Semantic Burden—but it carries it passively, in the sense that the transaction makes no use of it. The object's Semantic Burden was created by Rothko, curated by institutions, theorized by scholars, and experienced by the public. The private transaction extracts the financial premium this accumulated meaning generates without acknowledging, honoring, or contributing to the conditions that created it.

The Hollowed Object is the terminal form of this extraction. It is the object whose Semantic Burden has been systematically stripped through repeated speculative transactions—each of which extracted financial value while adding nothing to the object's narrative infrastructure—until what remains is a price point attached to a provenance claim, circulating in a private environment among buyers who experience it as an asset rather than artifact.

The Sovereign Object is the counter-form. As established in the OAC's study of the Aura Transaction—the analysis of what luxury consumes when it borrows cultural meaning without reckoning with its cost—the Sovereign Object is the artifact whose Semantic Burden is non-negotiable. It cannot be hollowed because its custodial architecture renders hollowing structurally impossible. The Anti-Sale Covenant prevents liquidation. The Custodian's Contract demands engagement. The Moral Weight Certification documents the labor that speculative substitution cannot replicate.

“The object that carries its own Custodian’s Contract is not a better investment. It is a different category of thing. It belongs to a different economy—one in which obligation, not liquidity, is the measure of value.”

Dark Mode cannot accommodate the Sovereign Object. The invitation-only environment, the sealed bidding architecture, the 365-day deal-making calendar that the trade now describes as the market's primary growth strategy—none of these formats have a mechanism for a work that arrives with binding custodial obligations attached. The whale economy needs objects that can be moved. The Sovereign Object refuses to move.

INSTITUTIONAL NECROPHAGY AS BUSINESS MODEL: THE STRUCTRAL ARGUMENT

The term Institutional Necrophagy requires precision. Necrophagy is the consumption of dead matter. In the biological register, it is a necessary ecological function: the breaking down of what has died to return its components to the living system. In the art market register, it is the systematic conversion of historical meaning—produced by dead artists, dead critics, dead patrons, dead institutions—into current financial value, without returning any of that value to the conditions that created it.

The Architecture of Extraction: As canonical works are crated for private vaults, the public's investment in their meaning is privatized, leaving the institutional record hollowed.

The private auction economy is necrophagy elevated to business model. Christie's does not need to invest in living artists' Labor Density to conduct a $200 million van Gogh private sale. It does not need to fund the institutional infrastructure that makes van Gogh comprehensible, teachable, or culturally significant. It needs only to facilitate the transfer of a physical object—whose value was entirely created by a century of public institutional investment—between two private parties, and collect its fee. The Cost of Stewardship is zero. The extraction is total.

The necrophagy critique extends beyond the major houses. The entire private auction ecosystem—Fair Warning, the emerging cohort of boutique private sale platforms, the 365-day calendar of off-market transactions that market insiders describe as the industry's new normal—is structurally dependent on the accumulated cultural meaning produced by public institutions. The Warhol sold at Clemente Bar was not made legible by Fair Warning's cuatorial judgment alone. It was made legible by the Museum of Modern Art, by every exhibition, catalog, and scholarly article that positioned Warhol as a canonical figure whose work carries cultural significance sufficient to command eight figures. Fair Warning consumed that significance. It did not produce it. It did not fund it. It did not acknowledge it.

“The private-auction economy is the most efficient value-extraction mechanism the art world has ever designed. It takes the public’s investment in cultural meaning and privatizes the return, perfectly and without remainder.”

This structural argument does not require moral condemnation of individual actors. Gouzer's conviction-based curatorial approach is sincere; his ecological commitments are documented; his aesthetic judgment is demonstrably sharp. The critique is not of the person but of the system his format perfects. Fair Warning, in its private auction iteration, is the most elegant formalization of institutional necrophagy currently operating in the market. Its elegance is precisely the problem. It makes the extraction beautiful.

WHAT THE MARKET REQUIRES: THE ANTI-DARK PROTOCOL

The counter-institutional response to Dark Mode is not transparency advocacy. Calls for greater disclosure, for public recording of private sale prices, for regulatory intervention in the auction house economy—these address the symptom while leaving the structural pathology intact. The problem is not that private transactions are invisible. The problem is that the transaction architecture—public or private—contains no mechanism for constituting the buyer as a custodian.

The Anti-Dark Protocol that the PLCFA framework proposes operates at the object level rather than the market level. It does not require regulatory reform of Christie's or Sotheby's. It requires the systematic deployment of three instruments that have already been proven in operation:

First: the Custodian's Contract, attached to the work at the point of commission or first transfer, binding every subsequent custodian to display obligations, community access provisions, and anti-speculative use restrictions. The Contract travels with the object. It survives every transaction, public or private. It cannot be removed by a subsequent buyer without the originating artist's consent.

Second: the Anti-Sale Covenant—the Monastic Veto encoded in legal form. The OAC's 1,825-day Anti-Sale Covenant is the operational model. A work governed by an Anti-Sale Covenant cannot be offered in a private auction environment during its Covenant term. The whale economy's liquidity requirement is incompatible with the Covenant's temporal lock. The object refuses the environment.

Third: Moral Weight Certification—the documentation protocol that makes the object's custodial claims verifiable and defensible. A certified work carries evidentiary documentation of its labor density, ethical provenance, community impact history, and material sourcing. This documentation cannot be produced retroactively by a private auction house. It requires the participation of the originating artist, the documenting institution, and the certifying infrastructure. The Cost of Stewardship is made visible and made legible.

“Dark Mode is only dark in the absence of the Anti-Sale Covenant. The object that carries the Covenant arrives in any environment—public or private—as something the transaction cannot consume.”

Together, these three instruments constitute what OAC terms the Anti-Dark Protocol: the counter-architecture to the private auction economy that does not require the private auction economy to reform itself. It requires only that artists, custodians, and institutions choose to deploy the instruments that already exist—and that the critical apparatus, as embodied in the PLCFA framework and its growing archive of institutional study, continues to name the difference between exclusivity and stewardship with sufficient precision that the market can no longer conflate them.

CODA

Dark Mode is not the art market's failure. It is the art market's achievement. It has successfully privatized the return on seventy years of public institutional investment in cultural meaning. It has built an architecture of exclusivity so refined that the thirty whales at the apex of the market can transact in conditions of near-total opacity without any accountability to the public infrastructure that made their purchases worth making. The velvet rope is seamless. The darkness is complete.

What the PLCFA framework confirms in this diagnosis is that the problem was never public versus private. It was always the presence or absence of the Custodian's Contract. Without it, a $195 million Rothko in a secret Christie's event and a $500 work at a public sale share the same structural category: the Hollowed Object, the asset that has been stripped of its obligation.

What the framework leaves structurally open is the question of scale. The three instruments of the Anti-Dark Protocol—Custodian's Contract, Anti-Sale Covenant, Moral Weight Certification—have been proven at the individual object level. The OAC's own archive, from L'Onde Silencieuse to the commission that deployed the 1,825-day Anti-Sale Covenant, demonstrates operational viability. What remains unresolved is whether any institution—a museum, a collecting foundation, a market regulator—will adopt these instruments at a scale sufficient to challenge the private auction economy's structural dominance.

The market has chosen its darkness. The question for 2026 and beyond is whether enough custodians—not collectors, not speculators, not whales, but genuine custodians—will choose the light of the Covenant instead.

Authored by Christopher Banks, Anthropologist of Luxury, Critical Theorist & Founder

Objects of Affection Collection

Office of Critical Theory & Curatorial Strategy

469 Fashion Avenue, 12th Floor, New York, NY 10018

RELATED OAC STUDIES

The following studies from the OAC archive speak most directly to the themes pursued in this paper.

The 2025 Market & Speculative Collapse

· The Singapore Protocol: How the Silent 95 Enacted the Monastic Veto

Anonymity, Aura & the Banksy Stress Test

· The Named Ghost: On the Reuters Unmasking of Banksy and the Ontological Value of Anonymity

· The Named Ghost: Part II — The Forensic Ledger

· The Wrong Face: On the Reuters Fact-Check and the Collateral Damage of an Unmasking

The Aura Economy & Institutional Extraction

· The Aura Transaction: On Louis Vuitton's Super Nature and the Ethics of What Gets Absorbed

Custodial Architecture & Stewardship Instruments

· The White Wall Paradox: Quantifying Consumption in the Age of Aesthetic Neutrality